Is Yotta Savings the Right Bank Account for You?

Written By: Nick Nguyen | Read full profile

This post contains affiliate links which means if you click on a link and choose to make a purchase I may receive a commission at no additional cost to you. You are not obligated to do so, but it does help fund these blogs in hopes of bringing value to you! See our disclaimer for more information.

Table of Contents

Pros

Okay, so around 3 months ago, two big personal finance gurus, Ask Sebby and Graham Stephan, started talking about this hot new bank account, Yotta Savings.

It follows this wonderful ‘no-lose’ lottery system model that favors those who put money in and KEEP IT THERE.

The entire aim of the account is to help people save and have an emergency fund for tough times. This is very similar to a system in the UK called Premium Bonds (you might of heard about this through Freakonomics).

They market the account as a chance to win $10 million dollars if you can match every single lottery ball!

Of course, as more people join, the chances of winning goes down, but the other prizes aren’t too shabby either! When you actually do the math, the more money you have, the higher your APY!

The second-tier prize is a Tesla, and the third-, fourth-, and fifth-tier prizes are split among all the winners for that week, which believe it or not, still wipes the floor with a traditional savings account. I mean, who wants to give up a chance to win a Tesla?

So let’s dive into the pros and cons. (We’ll do a more in-depth review of this after they’ve rolled out some new features in the next year).

PROS

So a lot of people think that it’s a scam. People with millions would obviously put their money in here and dominate chances to win $10 million. But to keep things fair, Yotta has a balance tier system for distributing extra tickets.

On balances up to $25,000, you can only get 1 ticket per $25 you leave into your account. For everything more than $25,000, you can only get 1 ticket per $150. This definitely helps smaller accounts have a shot at the grand prize!

Also remember that only the $5,000, $1500, and $1,000 are split among all the winning tickets. The $0.10 to $10 prizes are set values that you can still win. And trust me, if you’re able to win even a few of these prizes every month, you’ve crushed your traditional savings’ APY!

The more money you have in, the more chances and times you can win those smaller cash prizes! This is how they can advertise getting over 200x your current bank’s savings rates.

Is there really anything else we need to say here?

Their goal is to have you keep money in the account.

Why chip away at it with silly fees or minimums?

Just keep in mind, you’re only issued a lottery ticket for every $25 you have in there.

There’s a signup bonus if you use someone’s link or referral code (ours is NGUYENING if you want to support us).

The more people you refer, the more tickets you can earn! Just keep in mind that these tickets are only available for the next week’s drawings and only after they deposit some money into the account.

You even get 8 tickets on your first recurring deposit! This is why I love Yotta’s mission so much. Their goal really is to help people save as much money as they can!

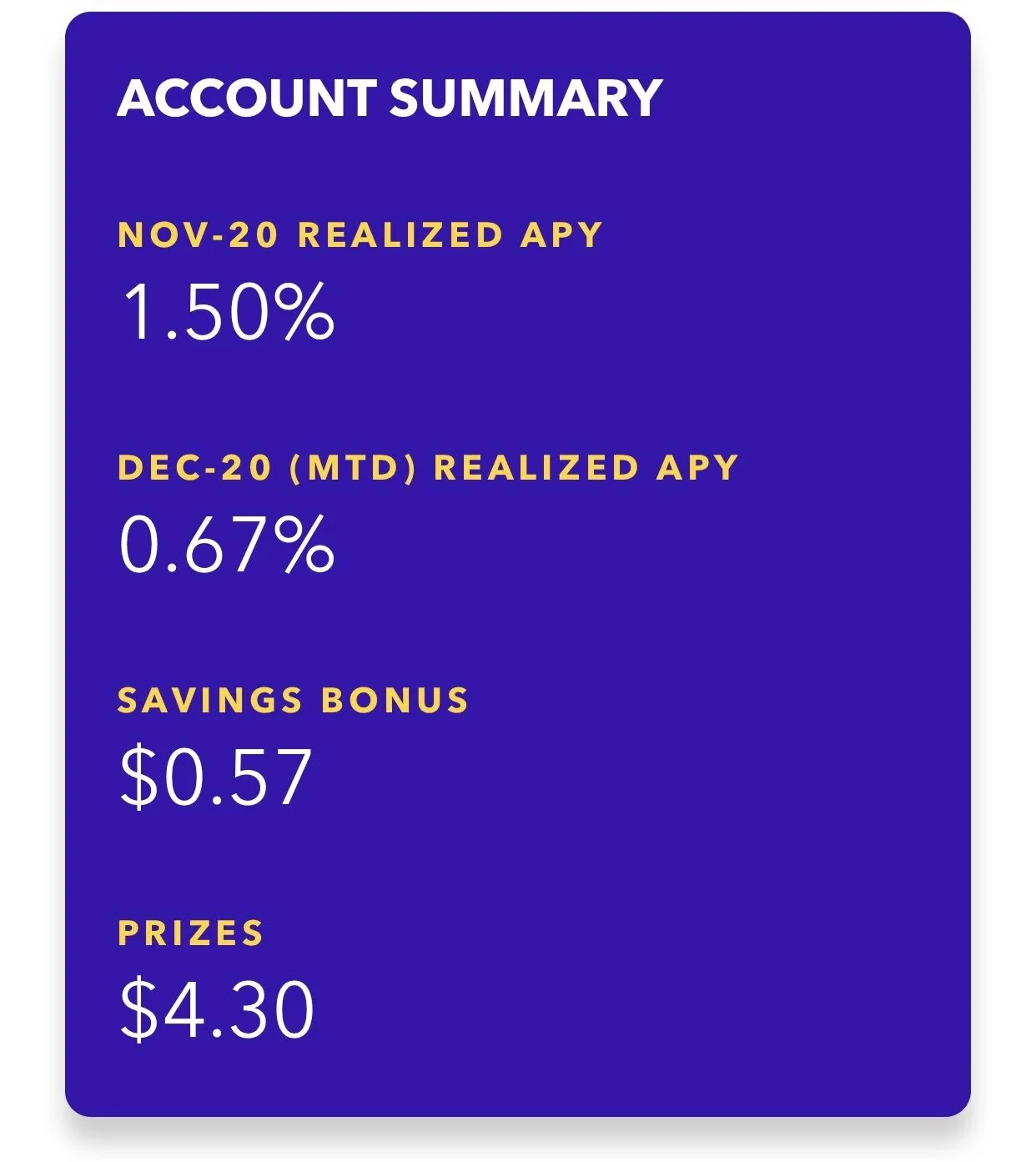

Yotta isn’t a bank, but it partners with other banks to have your money FDIC insured and earning a solid 0.20% APY* as of December 2020. If you bank with Credit Karma or Fidelity, this follows a very similar concept to their Savings and Cash Management Accounts.

*APY are subject to change.

I’m always skeptical about shady online banks nowadays. But, when I saw that a lot of different Youtube Personal Finance gurus had invested in the startup, I decided, why not?

Plus, it helps that it’s backed by the established startup accelerator, YCombinator.

The app is sleek and very simple to use!

The latest update from Yotta let you gift accounts to loved ones! So instead of giving them cash or a simple bank transfer, you could literally help them set up an account. What a perfect gift for birthdays, special occasions, or the holidays!

AND you still get your bonus referral if they set up their account through your gift and deposit some money. Talk about padding your lottery tickets for the week!

Now, you’ll see in a moment, one of my biggest Cons of the bank is how long it takes for the money to be transferred and updated in your Yotta balance. But, they’ve just added a waitlist for you to get a Yotta Debit card, which is a total game changer! Until that gets released on a large scale though, I’d be wary about putting your entire emergency fund in this account.

CONS

Like I was saying before, this is my biggest con. Of course, when you initiate a transfer in the app, you’ll still get your tickets for the week, even if the money hasn’t been sent yet, which is a plus.

Just keep in mind that if you need the money right away, it can take you anywhere from 3-7 days before you can finally get it into an account that you can withdraw the money from.

Luckily, they’re rolling out a Debit card, but as I mentioned, you’ll be a waitlist as of December 2020.

I mean...I get it. It’s to help reduce fraud, and most people only have 1 checking account anyway. But, if you’re like me, and you bin your money across multiple different accounts just to make sure you’re not overspending, it can be tough to play transfer hopscotch to get your money in the right bank so that Yotta can withdraw it.

Read more about how I use multiple accounts here: https://nguyeninglifestyles.com/nick/treat-yo-self-first-how-to-buy-whatever-you-want-and-not-feel-guilty?rq=treat

So it’s really tough to get a response. It will typically take a few hours to hear back from the support team, which makes sense since it’s a growing startup. BUT-

I will give them props for having a pretty solid FAQ list. I found a lot of the answers I was looking for on there, and it’s continually getting updated.

TAKEAWAYS:

So my takeaways are if you’ve got an extra $25,000 or more lying around or you’re looking to try to stash away some money in 2021 to really up your net worth, Yotta Savings is great.

Their concept is fun, and it really helps satiate those cravings to gamble with regular lottery tickets. Now you can do it all from the comfort of your home without having to pay a cent!

But, if you’re about to move your emergency fund in there that has a very strong possibility of being pulled on short notice...maybe this isn’t the best account for you, and you should go with a brick and mortar bank or one with an debit card, so you can always access that money from an ATM.

*Nguyening Lifestyles is not a registered financial service provider and does not give financial advice. All information in these posts are for entertainment purposes only. Nguyening Lifestyles is not liable for any actions or outcomes that transpired after your reading of the following post.